A look at what people across departments and programmes are currently doing, and what they can do, to handle their finances

(Photo: Karthik Ramaswamy)

Although India has a literacy rate of around 74%, it may surprise many that only 27% of the Indian population is considered financially literate. In fact, post graduates at 31% only do marginally better than the national average, while curiously, university students rank at the top at 43%. How do students at IISc fare in this regard? We interviewed several students across departments and programmes to find out.

For most UG and MTech students, saving is tough because the monthly stipend is too low. “My monthly stipend is Rs 5,000. Just the mess bill comes out to be more than that. My other expenditure is mostly on midnight food at Sarvam. We have no time to take up a part-time job. I know many who have less than a three-digit amount in their accounts,” says a second-year UG student. “The only way to earn extra is by volunteering for CNS [Centre for Neuroscience] experiments,” he adds while laughing. Annu Niraj, a second-year MTech student at the Centre for Product Design and Manufacturing (CPDM) says, “More than half of my stipend of Rs 12,400 goes into paying off an education loan I took for my BTech, and the rest goes in the mess bills. There is barely anything left for my expenditures, leave alone saving.”

Among PhD students, saving is also difficult for those who support their families with their fellowship. Brijesh Kanodia is a third-year PhD student in the Department of Physics. He says he spends around Rs 15,000 out of the Rs 35,000 he gets every month and sends the rest back home. Others don’t focus on saving for the future because they have other priorities: Pingal Pratyush Nath, a third-year PhD student at the Centre for High Energy Physics (CHEP) says he’ll think more about saving in the future when he has a higher-paying job. “Right now, most of my savings are spent on travelling. I plan a trip every two months or so. I’d go every month if I had the time and money.” Almas Siddiqui, a second-year PhD student in Civil Engineering, also says she’s trying to save in order to travel in the coming months: “I don’t think too much about the long term. I want to make the most of the present. Money comes and goes.”

Some PhD students say that they try to save in order to support themselves beyond the usual five years of a PhD in case they require longer to complete their work. Kiran Kolluru, a fifth-year PhD student in the Department of Physics, says, “The standard duration for students to complete their PhD requirements in my lab is six years. I’ve been saving 15,000 per month in an RD scheme for the past four years. I’ll use it to support myself if required.” Akshay C, another PhD student in his third year, says he knows many students in their sixth year who are struggling financially. “How is a student expected to do research with no financial stability?” he adds.

Some PhD students say that they try to save in order to support themselves beyond the usual five years of a PhD in case they require longer to complete their work

When we talk about savings, we usually mean putting our money in safe places that allow us access to our money any time, like a savings account, a fixed deposit (FD), or a recurring deposit (RD). But the tradeoff for the security and ready availability is that we earn low interest rates on the money we deposit. Investing money in real estate, stocks, mutual funds, cryptocurrencies, or commodities like gold and silver, for example, can lead to higher returns, but the stakes are higher: you could lose some or all of the original amount you invest. And not all students have an appetite for taking on that risk.

Debapriyo Chowdhury, a second-year PhD student from CHEP, says he wants to focus only on academics right now. “I save around 21,000 out of the 31,000 I get each month, and it stays in my savings account. I’ve never thought about investing it. I like doing science, and if I am getting paid for it, everything else will sort itself out, I believe.” Another common reason why students say they do not invest is the perception among many that investing is complicated and requires a lot of time and knowledge. “Investing is not my cup of tea. I don’t think I will be a good investor. I had never even thought of it before this interview,” adds Debapriyo. Almas says that she has colleagues who do invest, but she never considered it due to the risks involved. “I’ve heard that people can lose all their savings in the stock market. So I stayed away,” she says.

On the other hand, we have a fifth-year PhD student (who asked not to be named) at the Divecha Centre for Climate Change who started his own successful business in 2015 which is now being run by his family. He invests his money back into his own business, but has an opinion on why many students at IISc don’t invest. He says, “Unlike in a business or a job, PhD students have no profits to be earned or promotions to be rewarded based on their daily work. So they detach from the idea of growing their money and do not associate with the right people to get mentored in investing or starting a business.”

Tanveen Kaur Randhawa is a fifth-year PhD student at the Centre for Ecological Sciences (CES). They were unsure of how to begin investing until a friend advised them to start investing in mutual funds. “I thought it would be a complicated process. But you can simply download a brokerage app and start investing in mutual funds, just as we order food on Swiggy. But just as we check for restaurant ratings before ordering, you have to look at things like rate of return and commission charges of the fund before you invest.” They add that they put around 20% of all their savings in an FD, and the rest in mutual funds. “COVID-19 gave me a lot of time to think about my career trajectory. Even though I enjoy my work, I realised that this is perhaps not what I want to do all my life. I started saving in case my PhD runs over five years, which seems likely. I am also considering an alternate career path. Shifting towards another field or an industrial job is not always quick and smooth. I am saving so [that] I have some breathing space to assess my options and upgrade my skills as needed after my PhD,” they say.

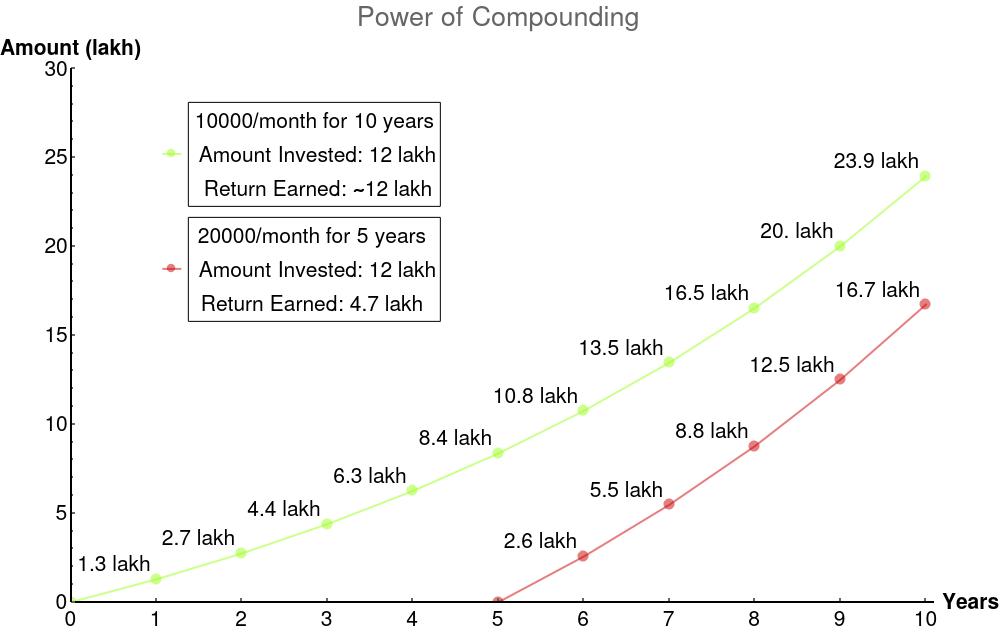

The graph shows the difference in earnings of two people who invest the same amount with an annual rate of return of 12.5%, but one starts five years later than the other. The early investor earns around 12 lakh, a 150% extra return compared to the 4.7 lakh earned by the late investor (Image: Faizan Bhat)

Some students swear by investing, rather than only saving, as a strategy to prepare for the future. Swapnil Shukla, a third-year PhD student at the Solid State and Structural Chemistry Unit (SSCU), has been investing directly in the stock market for around two years. “I started investing in the stock market during the COVID-19 lockdown after learning that my money in bank accounts is losing its purchasing power with time due to inflation,” he says. The fellowship amount of a Senior Research Fellow (SRF) in 2010 was Rs 18,000, which has increased over the years to Rs 35,000 presently. But if we consider inflation, Rs 18,000 in 2010 is the equivalent of about Rs 39,070 today. So leave alone any income growth, the fellowship hike over the years has not even kept up with the inflation rate. Swapnil adds, “I decided to invest in the stock market to get higher returns. It was scary in the beginning as I was a complete novice. I would listen to a bulletin on some business news channel in the morning and buy stocks according to the advice of their experts. Then if the stock price fell, I would panic and sell it immediately at a loss. With time, I realised that this is not the correct way to invest in the long term. Buying shares on your own can be risky, especially if one doesn’t have a strong understanding of the stock market or the patience required to handle the market volatility. I’ve gotten more confident over time and invest more responsibly now,” he says.

For students looking to grow their savings, Balachandran Ramiah, a financial expert with a PhD in Marketing, Business, and Public Policy from the University of Pennsylvania, has some tips. “The safest and most practical way for a student to invest is through the Systematic Investment Planning (SIP) schemes offered by mutual funds. Through an SIP, you can deposit a certain amount at regular intervals, and the mutual fund manager will invest it in the stock market for you,” he says. According to him, it is advisable to invest at least 20% of one’s salary, and students with no additional responsibilities can try to save around 30%. He also suggests investing in a health insurance policy: “The premium charged by insurance companies increases as you age, and you can also get broader coverage if you’ve no existing ailments. So, it is more economical to buy when you’re young and healthy.”

Now is as good a time as any to invest, he says, so that your money compounds with time. “In the long run, it’s not the amount you invest but the time you invest it for that matters a lot more. So the earlier you start, the better,” he says.

Faizan Bhat is a PhD student at the Centre for High Energy Physics and a science writing intern at the Office of Communications, IISc